Our November nickel press release highlights that smelting activity increased by 3.2% month-on-month in October, rebounding from its lowest level in nearly a year and a half in September. Nonetheless, at 17.6%, Earth-i’s metals production monitoring index, SAVANT, is still 3.5% higher for nickel than the same period a year ago, and 2.9% above the 3-year average for October.

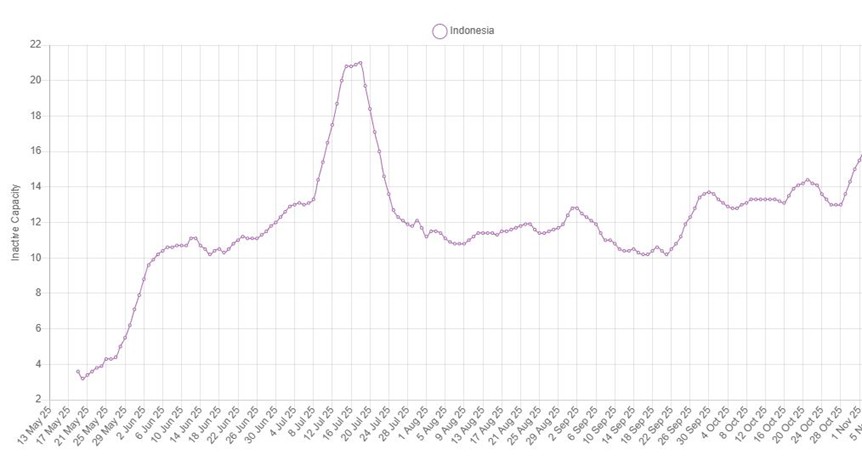

Following a particularly weak reading in September, activity in China bounced back so that the country level inactive capacity series registered an average of ‘only’ 23.6% across October, although this was still 14.6% higher than a year ago and 10.2% above the 3-year average. An improvement here was partially offset by a softening of activity in Indonesia where smelting activity fell by 2.2%, as deduced by a rise of the same magnitude in the archipelago’s inactive capacity series. Indeed, at an average of 13.7%, the world’s largest nickel producer registered the second weakest reading since March 2024, exceeded only by July’s 13.9%.

Fig I: Indonesia Inactive Capacity Index, May 2025 – Present

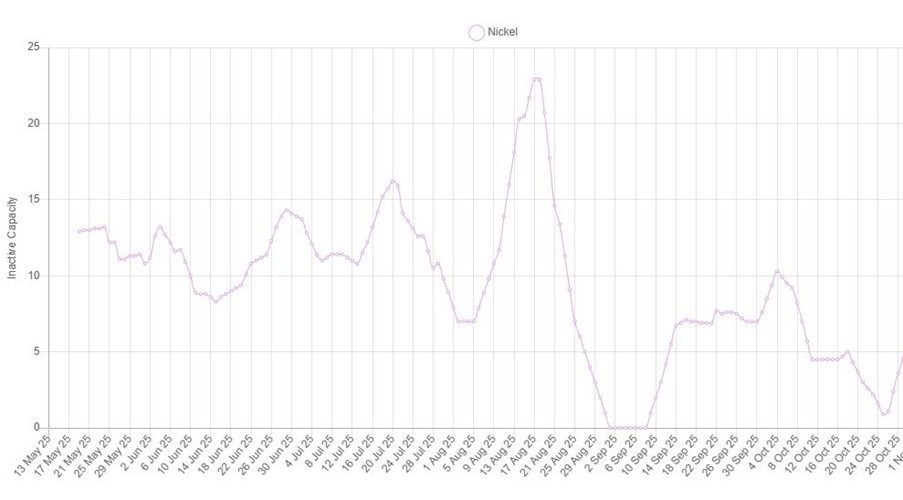

Looking at market dynamics across the metal grades, the ferronickel segment remains the weakest. Despite activity at operations producing high-purity nickel-iron alloys increasing by 6.9%, the inactive capacity series still recorded an elevated 33.8%, indicating that a third of all capacity in this segment was offline in October. Conversely, the improved performance of plants in China helped boost nickel pig iron (NPI) activity by 3.8%, so that the inactive capacity sub-index for the lower-grading ferroalloy fell to 19.2%. Nevertheless, activity at Class I operations producing LME deliverable cathodes, pellets, briquettes or rounds (as well as non-deliverable powders) continues to be much stronger than in the lower grades, with inactive capacity averaging only 5.4%. This is primarily due to this segment’s concentration at a relatively small number of large sites, so that strong operating profiles at Jinchuan’s eponymous 150 kt/a smelter in Gansu and Nornickel’s 200 kt/a Nadezhda Metallurgical Plant are highly influential.

Looking at market dynamics across the metal grades, the ferronickel segment remains the weakest. Despite activity at operations producing high-purity nickel-iron alloys increasing by 6.9%, the inactive capacity series still recorded an elevated 33.8%, indicating that a third of all capacity in this segment was offline in October. Conversely, the improved performance of plants in China helped boost nickel pig iron (NPI) activity by 3.8%, so that the inactive capacity sub-index for the lower-grading ferroalloy fell to 19.2%. Nevertheless, activity at Class I operations producing LME deliverable cathodes, pellets, briquettes or rounds (as well as non-deliverable powders) continues to be much stronger than in the lower grades, with inactive capacity averaging only 5.4%. This is primarily due to this segment’s concentration at a relatively small number of large sites, so that strong operating profiles at Jinchuan’s eponymous 150 kt/a smelter in Gansu and Nornickel’s 200 kt/a Nadezhda Metallurgical Plant are highly influential.

Fig II: Class I Nickel Inactive Capacity Index, October 2024 – Present At a regional level, Asia & Oceania continues to be the strongest geographical grouping being the only one with an inactive capacity sub-index reading in single figures, at 6.1%. Meanwhile Europe is weakest, where it is no coincidence that four out of the five active facilities are ferronickel smelters. However, a jump in the inactive capacity series to 80% in October was in large part due to a patchy operating profile at the continent’s only Class I nickel-producer, namely Boliden’s 45 kt/a Harjavalta.

At a regional level, Asia & Oceania continues to be the strongest geographical grouping being the only one with an inactive capacity sub-index reading in single figures, at 6.1%. Meanwhile Europe is weakest, where it is no coincidence that four out of the five active facilities are ferronickel smelters. However, a jump in the inactive capacity series to 80% in October was in large part due to a patchy operating profile at the continent’s only Class I nickel-producer, namely Boliden’s 45 kt/a Harjavalta.