At LME Week last month, the Exchange sprung something of a surprise by announcing the establishment of a subsidiary in Dubai to act as price administrator for the introduction of ‘green’ premiums. However, while the concept has been floated for some time now, initiatives like the Copper Mark and the LME’s own responsible sourcing requirements have made it something of a moot point, with ESG assuming the importance of ‘table stakes’. So why could now be the moment to give this sustainability project the shot in the arm it needs?

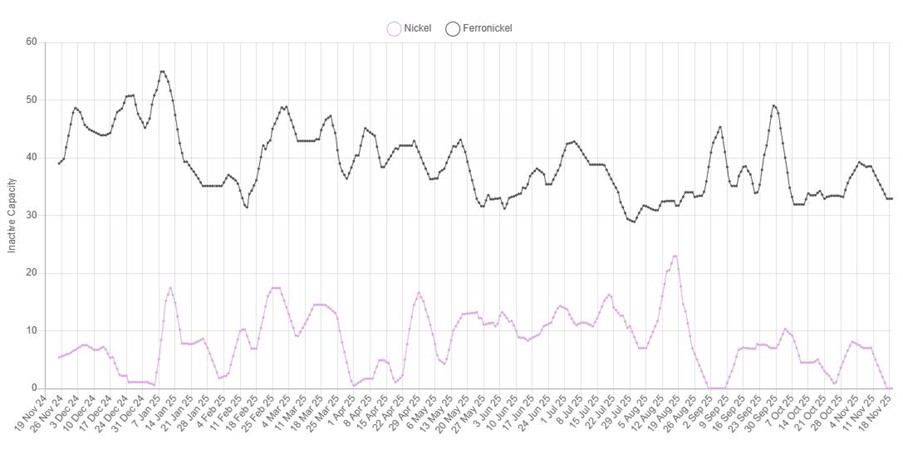

The nickel market could hold the key. When we unveiled the ‘nickel active capacity’ feature of the SAVANT platform back in the middle of the year in our article ‘‘Are we approaching peak nickel?’, we focused on nickel pig iron (NPI) in China and Indonesia to support our hypothesis. Over the course of the last 20 years NPI has usurped ferronickel in many supply chains as its lower cost of production has rendered traditional Class II plants obsolete, particularly in Europe. This explains why the SAVANT inactivity capacity series for the higher-quality Class II ferroalloy has remained stubbornly above 30% for the last year (see Chart 1).

Chart 1: Nickel (Class I) & ferronickel (Class II) inactivity capacity series, Nov 2024 – Present

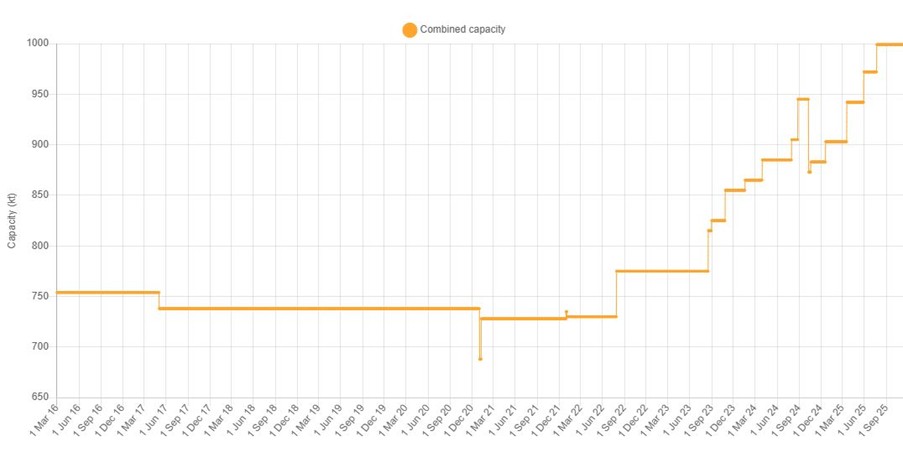

By contrast, operations producing Class I nickel – metal that can be delivered onto the LME – have seen their inactive capacity reading as a collective fall close to zero on several occasions over the same period. Firstly, we should say that this is not the result of closures that have led to a ‘last man standing’ situation. In fact, quite the opposite is true as there has been a surge in Class I smelting capacity since the middle of 2023 (see Chart 2).

Chart 2: SAVANT nickel cumulative smelting capacity, March 2016 – Present

Much of this has been due to the conversion of NPI plants in Indonesia to instead produce nickel matte, especially in the industrial parks at Morowali and Weda Bay. This evolution is well illustrated by Huayou Cobalt, one of the vanguards of China’s push into new technologies and hi-tech manufacturing, specialising in cathode-active materials (CAM). On the company’s website they show a (highly idealised) schematic[1] of what is now labelled the ‘Huake High Nickel Matte Smelting Project’, but which started as 4 rotary kiln electric furnace (RKEF) lines producing NPI in mid-2022, before switching to high grade matte later that year. But I hear you ask – how do plants like this, with their well-publicised disregard for ESG concerns, meet the LME’s mandate for ISO 14001 certification as part of the Exchange’s responsible sourcing requirements?

Looking at the LME’s approved nickel brands provides the answer. There is only one registered to Indonesia – PT CNGR Ding Xing New Energy’s full plate cathodes. Meanwhile China has 8 active listings, of which ‘HUAYOU’ and ‘HUAYOUgx’ do not need much investigation! Nor are Huayou Cobalt alone – CNGR New Energy Science, majority owners of the ZhongTsing New Energy plants in Morowali Park, also have a listing under ‘CNGR’, while GEM Co Ltd. has ‘GEM-NI1’ and ‘GEM-NI2’. In a form of green washing, these companies ship the intermediary matte produced in Indonesia to facilities in China where they are refined into electrolytic nickel, before being delivered back out into the LME network. In so doing the owners are sticking their tongues out at the Exchange’s responsible sourcing rules.

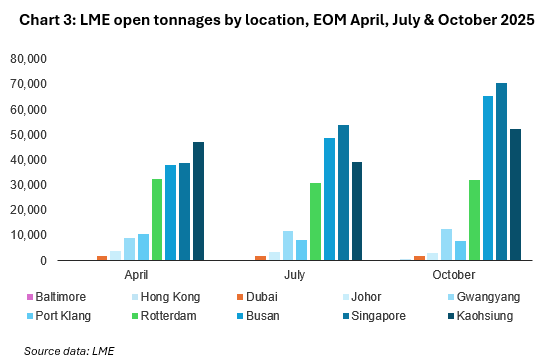

But with OEMs such as BYD and Wuling favoring lithium-ion phosphate batteries to nickel-manganese-cobalt designs in their EVs, the CAM manufacturers are becoming increasingly dependent on the LME as the market of last resort to offload expensive excess raw materials and free up capital. This is becoming more and more visible as cathodes from China accumulate rapidly in LME warehouses across Asia (see Chart 4).

Source data: LME

Indeed, looking at the Exchange’s country of origin data, 70% of all open tonnage at the end of October was Chinese material. And herein lies the opportunity with which the LME could redress the balance – namely by introducing green premiums under different criteria, in combination with digital platform Metalshub, it could effectively segregate this material from consumers keen to tout their own ESG credentials. For these companies, instead of more than 255,000 tonnes of available metal on the Exchange there would instead only be around 34,000 tonnes, excluding material from Russia and Indonesia as well.

That should create enough scarcity for a healthy and enduring green premium.

Read our November 2025 press releases on the global copper and nickel markets for more insights.

[1] https://www.huayou.com/en/products/indonesia-nickel-industry