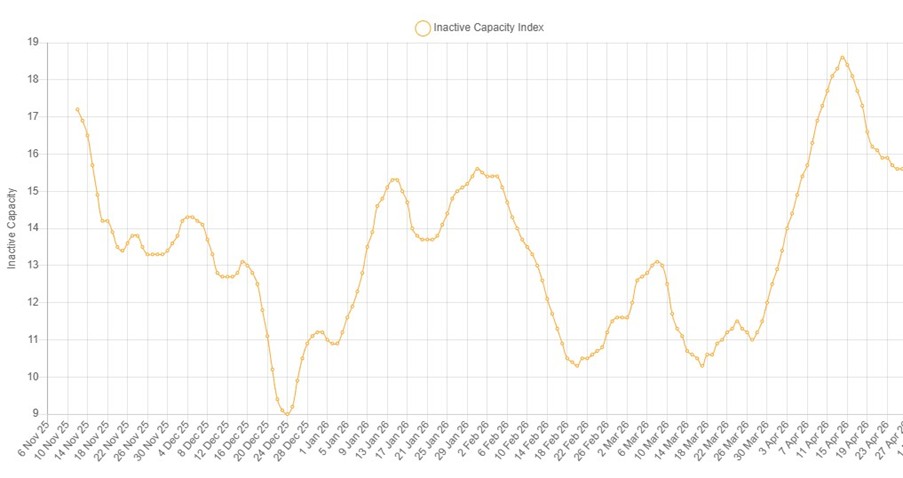

Global smelting activity fell sharply, but not unexpectedly, in April our SAVANT Global Copper Monitoring Index has demonstrated, recording its largest month-on-month decline in more than 3 years. The trend was widespread, with every region except Asia & Oceania registering a rise in inactive capacity, so that the global inactive capacity series increased by 4.7% to 16.3%.

Fig I: SAVANT Global Inactive Capacity series, November 2025 – Present

China was the region that saw the greatest shift with the country level inactive capacity series gaining 8.1% to 12.0%, its highest reading since June 2024. However, this should not be seen as unusual – or indeed interpreted as a second-round effect stemming from the conflict in the Middle East – with ‘maintenance season’ in the second quarter of the year. It is customary for smelters to take downtime to coincide with the seasonal lull in the production cycle between Q1 deliveries to tube manufacturers, for the assembly of air conditioners ahead of summer in the northern hemisphere, before orders ramp up again in Q3 from wire rode producers ahead of the peak in construction activity in autumn.

More pertinent were developments in the Rest of World (RoW), where inactivity collectively rose by 1.8% to 19.9%, or almost a fifth or total capacity. This was in part due to a lack of operating signals from 280 kt/a Sarchesmeh and 120 kt/a Khatoon Abad in Iran that we previously noted had been observed going offline in late March and early April respectively, although SAVANT monitoring indicates that both plants have been active again since the third week of April. Similarly, the 300 kt/a Mount Isa smelter returned at the end of the month, seemingly after a 16-week shutdown for the regular rebricking of its ISASMELTTM furnace.

Meanwhile in Europe, the continent’s inactivity series breached 10% for the first time in six months, rising by 4.5% to 10.7%. This was the result of generally patchy operating profiles across several plants, including 230 kt/a Harjavalta in Finland and 450 kt/a Hamburg in Germany, rather than a prolonged shutdown at any site in particular. Smelting activity also declined in North and South America, by 1.4% and 6.6% respectively, with the latter driven by a 9.4% increase in inactivity in Chile. Once again, it was patchy operating profiles that were responsible – this time at 450 kt/a Chuquicamata and 150 kt/a Chagres. Finally, activity levels were unchanged in Africa, with the Mother Continent’s inactive capacity series remaining steady at 10.4%.

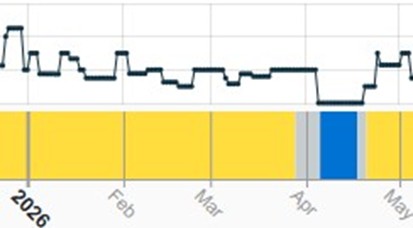

Fig II: Khatoon Abad smelter, January 2026 – Present

Yellow = active, blue = inactive, grey = no reading

See more about Earth-i’s SAVANT Global Copper Monitoring Index here.