Nickel smelting activity fell back in May according to our SAVANT metal monitoring index, with the global inactive capacity series increasing 2.6% to 14.9%. Gains of 1.7% and 6.2% in Indonesia and China respectively, which together account for over three quarters of total industry capacity monitored by SAVANT, were the primary drivers despite strengthening downstream markets and rising prices for stainless steel products.

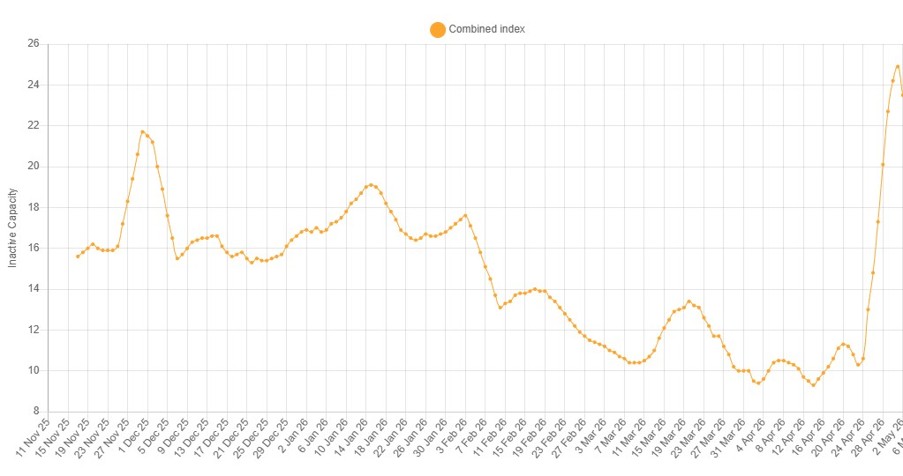

Fig I: SAVANT Indonesia & China combined inactive capacity, November 2025 – Present

For both geographies the averages for the month do not tell the full story. In Indonesia, the world’s largest nickel producer, the country level inactive capacity series averaged 12.7% across the month, up from 11% in March. However, in the final week of April the percentage of capacity observed as inactive on the SE Asian archipelago registered five days above 20% (see Fig 1), before falling slightly on 30th April to ‘only’ 18.6%. While the well-publicised issues at PT Huadi Nickel Alloy in South Sulawesi has seen output restricted to the Phase 2 operating line at the 64 kt/a nickel in NPI facility, changes in activity at a number of sites within the Morowali Industrial Park were more responsible for this volatility.

Similarly in China, while average inactive capacity for the month was 15.6%, up from 9.5% in March, the final week saw 5 days above 40%. This weakness was mainly due to a (temporary) lack of activity signals at the behemoth 190 kt/a nickel in NPI Shandong Xinhai plant that accounts for more than a fifth of country level capacity. In addition there were also outages at the 40 kt/a Jingan NPI and 8 kt/a Lianyungang Huale Alloy plants. But potentially the most significant stoppage, which has stretched into May, is that at the remote 8 kt/a Kalatongke smelter in Xinjiang which produces matte for the refining of high-purity nickel at the nearby Fukang refinery.

Together with a lack of operating signals at 70 kt/a Sudbury INO, the outage at Kalatongke helped push the class I nickel inactive capacity sub index up by 4.7% to 7.8%, its highest reading since August last year. The NPI sub index also rose, by 2.9% to 14.5%, so that of the metal grades only ferronickel saw an increase in activity, of 3.1%. This was in large part due to strength in the operating profiles of the three Brazilian smelters and 27 kt/a Onca Puma in particular. Nontheless, with the industry in Europe still paralysed by high electricity costs, in combination with extended closures at other operations like 32 kt//a Falcondo in the Dominican Republic and 22 kt/a Tagaung Taung in Myanmar, the ferronickel inactive capacity sub index remains the highest of the three grades at 31.2%.