Our latest steel production press release shows that Canadian steel production is down as US tariffs bite, but resilience remains with support from the domestic market

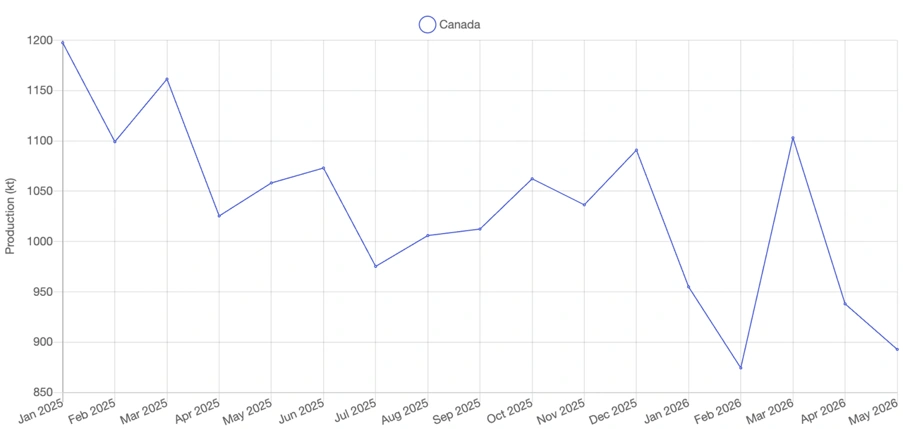

Canada’s steel production output slumped in May, down 15% on May 2025 and 14% down on the year-to-date figures for the same period last year, according to Earth-i’s SAVANT Global Monitoring Index.

The imposition of the April 2025 Section 232 mandate’s universal 50% tariff and the April 2026 Section 232 tariff Implementation Updates applying to derivative steel products, have been dramatic in slowing steel exports to the US. Over the course of 2025, Canadian steel imports to the US dropped by 31% and is tracking a whopping 55% down year to date (to end March 2026) according to the US International Trade Association.

However, the impact of the US Tariffs on Canada’s overall steel production has been less dramatic than might have been anticipated, so far.

Fig 1 – Canadian Production Activity 2026: May 2025 to May 2026

Source: SAVANT

The downward trend is not being felt uniformly across all plants in the country.

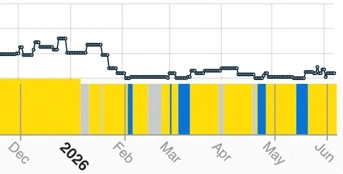

Algoma is the standout driver behind the year-to-date fall having been highly exposed with around half of its primary commercial products traditionally sold to the US. It subsequently brought forward closure of its blast furnaces (January 2026) and is progressively ramping up its EAF units although still well below previous activity levels.

Fig 2 – SAVANT Activity Index for Algoma

Aside from Algoma, most plants have been surprisingly resilient.

ArcelorMittal’s Montreal steel plant specialises in long steel products which are sold to Eastern Canada’s protected domestic construction and civil infrastructure markets rather than relying on the flat rolled products sold to the US. April and May have been softer months leaving year-to-date production down around 8%, according to SAVANT.

Similarly, while ArcelorMittal’s Dofasco core business relies on Harmonized Tariff Schedule of the United States (HTSUS) Chapter 72 flat-rolled steel, its long-term procurement agreements serving Ontario’s local automotive corridors (accounting for most of its steel market) provide domestic market support allowing it to track 3% up year-to-date SAVANT data is showing.

The other key producer, Stelco’s Lake Erie steel, has also pivoted towards the domestic market capturing the supply vacuum left behind as expensive US steel imports withdrew. So far, this strategy appears to be having some success demonstrated by an estimated 9% increase in year-to-date production (SAVANT data).

Together with the recent Section 232 tariff Implementation Updates, Canada’s steelmaking outlook remains challenging especially for Algoma, although mills able to capitalise on their domestic market focus such as ArcelorMittal’s Dofasco and Montreal plants and Stelco, have been reasonably sheltered so far.

See more about Earth-i’s SAVANT Global Monitoring Index by industry sector here.