As the war in Iran enters a precarious ceasefire and oil prices tumble, there is hope that the most dangerous period of the conflict may have passed. Nonetheless the ramifications for the global economy will likely last far longer, especially if safe passage through the Straits of Hormuz remains elusive. And for as long as this is the case, energy prices are likely to hold at elevated levels. So what impact is this having on those sectors of the commodity complex monitored by SAVANT?

For the copper industry much of the attention has focused on the supply crunch in sulphur potentially curtailing production from solvent-extraction electrowinning (SXEW) mines, particularly in the Copperbelt. We tend to believe this is overstated as many are owned by Chinese State-Owned Enterprises (SOEs) such as CMOC and CNMC who have the financial capability and global reach to secure alternative sources. In the midstream, commentary has focused on rising energy prices and the propensity for these to further pressure smelter economics, already reeling from record low TC/RCs.

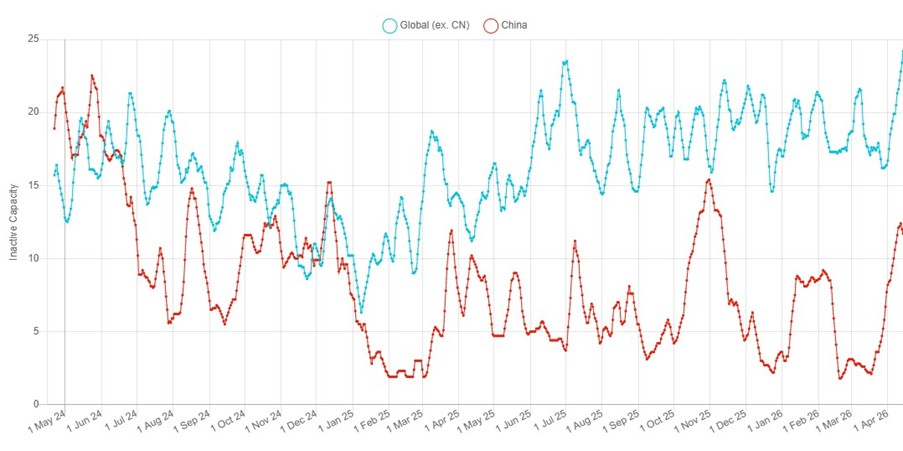

Indeed, recent data showing a spike in the inactivity series for both China and Rest of World (RoW) would seem to corroborate this … or do they?

Chart 1: SAVANT China and Rest of World inactive capacity series, May 2024 – Present

In reality, ‘smelternomics’ are more sensitive to the revenue side of the equation than electricity costs, as the most important reactions in both the flash and bath processes use the fuel value of the feed material to smelt the charge, with the energy coming from the oxidation of sulphur contained in concentrates.

So, while power is typically the largest cost category at around a quarter of total operating expenditure, this is actually less than the income received from sales of sulphuric acid, which even in more ‘normal’ conditions account for around a third of total income (the precious metals’ revenues we examined in our previous post, ‘All that glitters, … but it’s not gold’ typically only contribute around 10%, the same as ‘free metal’). And as a smelter will produce around three tonnes of acid for every tonne of copper, leverage to the acid price is much greater than to gold or silver. Therefore, with prices doubling over the last fortnight, acid will have suddenly become by far the most important revenue stream for most plants, especially considering the negative treatment and refining charges (TC/RCs’) prevailing in the market.

So why then would we see a drop in activity if smelters are seeing their profitability improve due to the dislocations caused by the war?

Firstly in China, there is a consistent pattern of higher inactivity in the second quarter each year as plants conduct routine maintenance. This coincides with a seasonal lull in the production cycle between Q1 deliveries to tube manufacturers for the assembly of air conditioners ahead of summer in the northern hemisphere, before orders ramp up in Q3 from wire rode producers ahead of the peak in construction activity in autumn, often augmented by back-loaded POs from the State Grid.

What is interesting is that, so far at least, shutdowns have been concentrated in the south of the country, in regions whose economies are more export-orientated than in the north.

Simultaneously, looking at smelting activity in the RoW, the largest declines have been seen in the Atlantic economies of Europe and North America, which together account for around half of global GDP.

Could copper smelters be the canary in the coal mine for the global economy as ratcheting energy prices and subsequent inflation threaten to pull many economies into recession?

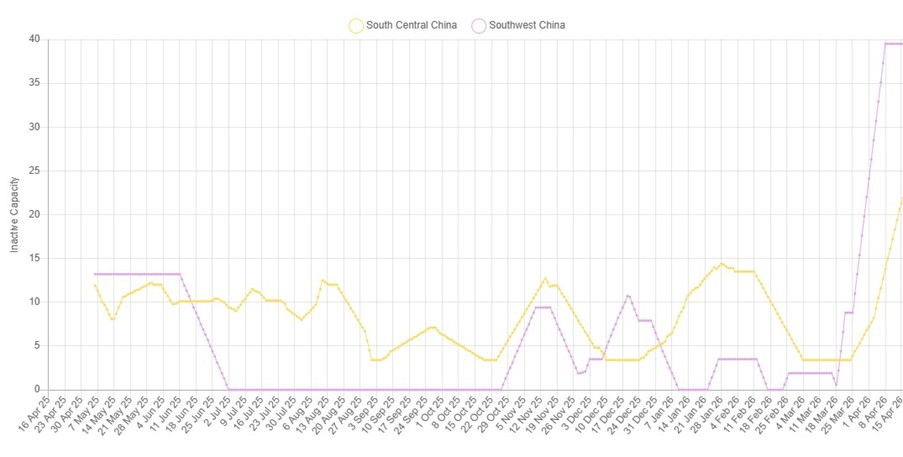

Chart 2: SAVANT Southwest and South Central China inactive capacity series, April 2025 – Present

But such are the perverse incentives playing out in the market at present that it would seem overly simplistic to isolate such a causal relationship. The imposition of export restrictions on sulphuric acid by countries including China, as they seek to protect their agricultural sectors by prioritising fertilizer supply over exports, could send acid prices in international markets even higher still.

Back in January 2025 we hypothesized that Chinese smelters would follow the economic pragmatism of former Chairman Deng Xiaoping by trying to inflict as much pain as possible on overseas competitors by taking TC/RCs down to levels that would render older, less efficient capacity uneconomic. The spread that has since become entrenched between inactivity in China and RoW shown in Chart 1 is evidence this strategy is working. But by restricting exports of acid Beijing could be handing a leg up to smelters offshore, both increasing prices in the international market and reducing them domestically.

We may be approaching an acid test moment … on several fronts.