Our SAVANT Global Metals Monitoring Index showed that global smelting activity improved in February, with the percentage of total capacity registered as inactive falling by 2.2% to 12.1% from a record high for January. Nevertheless, activity remains weak by comparison to previous years, with the global inactive capacity series 4.7% above the 3-year average, so that active tonnage monitored by SAVANT is 595kt lower than January 2025’s high of 22.3Mt.

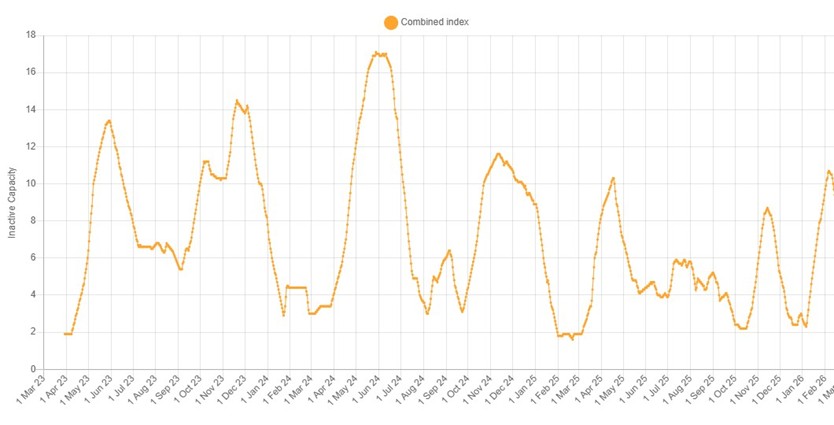

At a regional level China continues to outperform the Rest of World (RoW) with the country’s inactive capacity series falling by a larger 2.5% to just 5.0%. This is consistent with seasonal patterns driven by the timing of Chinese New Year, as well as the requirement to have product ready for semi fabricators to take advantage of the uptick in economic activity that comes with the end of winter in the northern hemisphere. The high prices that have weighed on demand since the beginning of the year appear to still be having an impact, with smelting activity in the powerhouse East and South Central regions, that together account for 43% of country level and 30% of global capacity monitored by SAVANT, 2.4% and 3.3% respectively below their 3-year averages.

Fig I: SAVANT East & South Central China combined smelting inactivity, March 2023 – Present

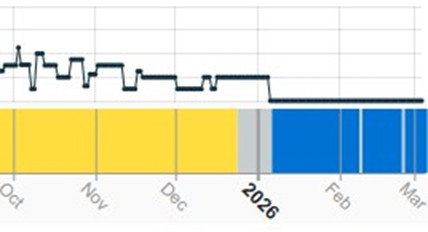

Although the RoW continues to lag China with an inactive capacity reading of 18%, all regions except for Asia & Oceania recorded an improvement in smelting activity in February. Here the 1.3% rise in the inactive capacity sub-index was primarily due to a lack of operating signals from the 300kt Mount Isa plant in Queensland, Australia, consistent with the regular maintenance requirement to replace the furnace’s 60,000 refractory bricks every four years.

Africa was the strongest performer over the month, where the inactive capacity series fell by 5.3%, helping the Mother Continent move ahead of South America, which is now the region with the highest percentage of inactive capacity at 25%. Europe remains the region with the most active smelters on average, with just 4.1% of capacity inactive across February so that at almost 2.65 Mt, active tonnage is running almost 100,000 tonnes above the 3-year average.

Meanwhile – and similar to last month – it should again be noted that SAVANT monitoring has not detect any interruptions to smelting in Iran, with both Sarchesmeh and Khatoon Abad showing consistently active operating signals, despite the war in the country.

Fig II: Mount Isa smelter, October 2025 – Present

Yellow = active, blue = inactive, grey = no reading