Our July nickel update saw smelting activity across the nickel industry falling in the second quarter of 2026, according to our SAVANT metals monitoring platform, with global inactive capacity increasing 4.0% q/q to 18.4%.

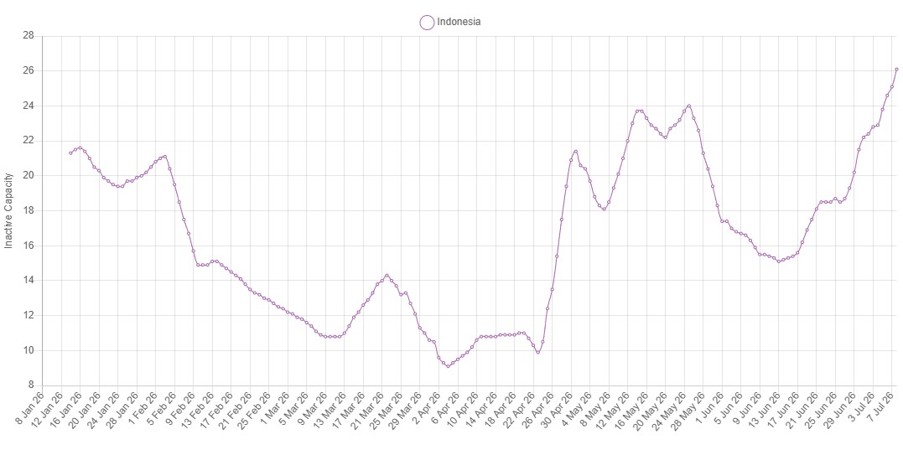

Within the period, and at an average of 21.4%, May registered the highest monthly reading in two years. This was primarily due to weakness in Indonesia, where a reduction in mining quotas (RKAB) for this year to ‘only’ 260 – 270 million tonnes has led to reduced ore feed availability, in turn forcing smelter operators to cut back production. As a result, the country-level inactive capacity series for the world’s largest producer of nickel now stands at 17.2%, a rise of 8.4% y/y. This corroborates comments from industry association FINI who asserted at last month’s Indonesia Critical Minerals Conference & Expo 2026 in Jakarta that capacity utilisation across class II producers had recently fallen by 10%.

Fig I: SAVANT Indonesia inactive capacity, January 2026 – Present

SAVANT monitoring shows that the most impacted sites look to be those in Central and Southeast Sulawesi. In addition, several facilities in which Tsingshan Group has an ownership interest at the Weda Bay Industrial Park (IWIP) have been registered as inactive in recent weeks, as the company looks to conserve energy to instead prioritise production of higher margin aluminium at its neighbouring 250 kt/a Juwan plant, also located in the IWIP.

Fig II: Selected IWIP smelters, April 2026 – Present

Yellow = active, blue = inactive, grey = no reading

At the same time, smelting activity has generally been weak across the rest of the world, so that Q2 global inactive capacity was both 4.2% higher y/y and 2.8% above the three-year average.

Activity was weakest in Europe, where the inactive capacity series rose by 13.5% to 72.7%. The region has long been that with the lowest level of smelting activity, as high electricity prices have rendered its ferronickel plants at Larymna in Greece, Ferronikeli in Kosovo and Kavadarci in North Macedonia uneconomic compared to cheaper NPI operations in Asia.

At the same time the war in Ukraine has meant that SAVANT has seen no production at Pobuzhskiy since October 2022. However, recent weakness has been more attributable to a patchy operating profile at the 45 kt/a Harjavalta smelter in Finland, Europe’s only nickel matte producer. This also contributed to a 10.2% fall in global activity at Class I producers globally, the first time the series has recorded a reading in double figures since Q2 2024.

Only in Africa did activity increase, although due to the small number of operating sites on the Mother Continent, readings here can be more volatile than in other regions.