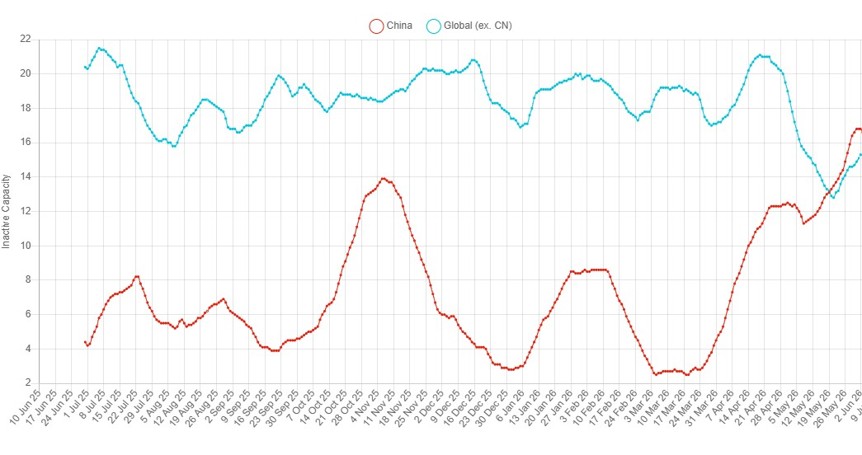

Our June copper smelting bulletin is showing that regional acid price differentials fuelled diverging behaviour between copper smelters in China and the Rest of World (RoW) in May, exaggerating seasonal patterns. Smelting activity in China fell by 2.5% from April so that the percentage of capacity registered as inactive rose to 14.5%, the highest reading in almost two years.

At the same time activity in RoW rose by 5.7%, the largest gain since December 2023. Consequently, smelters in China are now on average less active than those in other jurisdictions; a rare situation that has been seen fewer than ten times this decade.

Fig I: SAVANT China and RoW Inactive Capacity series, 21-day moving average, June 2025 – Present

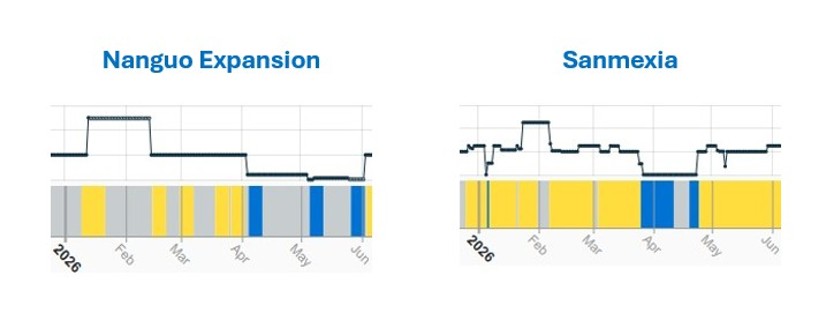

As we commented last month, it is not unusual for smelting activity to decline in China during the second quarter – often dubbed ‘maintenance season’ – but this year the effect has been particularly pronounced, with the country level inactivity series surging from just 3.9% only two months ago. Much of the increase can be attributed to the operating performance of plants in the South-Central region, where active capacity fell from 2.86 Mt in the last week of March to just 2.16 Mt a month later. Notable contributors to this reduction have been the smelters at the 275 kt/a Nanguo expansion and 300 kt/a Sanmexia. With headline TC/RCs deep in negative territory, less accessible inland plants with higher transport costs have been especially reliant on revenues from by-product sulphuric acid, and to a lesser extent precious metals, to remain economic. However, it would seem no coincidence that sulphuric acid prices in the provinces of Guangxi and Henan have been among the lowest in China since the unofficial ban on exports was introduced last month.

Fig II: Nanguo Expansion and Sanmexia smelters, January 2026 – Present

Yellow = active, blue = inactive, grey = no reading

Yellow = active, blue = inactive, grey = no reading

The withdrawal of Chinese cargoes of sulphuric acid from the international market has also been significant, as other countries have become increasingly reliant on these shipments in recent years to alleviate their own structural deficits. As such prices for acid are making strong gains in many regions, even if they are not (yet?) back at 2022 levels following the Russian invasion of Ukraine.

Therefore, smelters in other regions – and particularly those in the northern hemisphere where downtime for maintenance usually takes place soon to coincide with workers’ summer holidays – are currently incentivised to increase capacity utilisation. It is therefore not surprising that smelting activity increased in all regions outside China, except for Africa, where although the Mother Continent’s inactivity series rose to 17.7%, this still remains well below the three-year average for May at 25.9%.

Notable among facilities that have registered strong operating profiles in recent weeks have been smelters in the US, where sulphuric acid prices had risen to more than $400/t CFR US Gulf in early May, from only $155/t before the war in Iran.

Fig II: La Caridad and Miami smelters, January 2026 – PresentYellow = active, blue = inactive