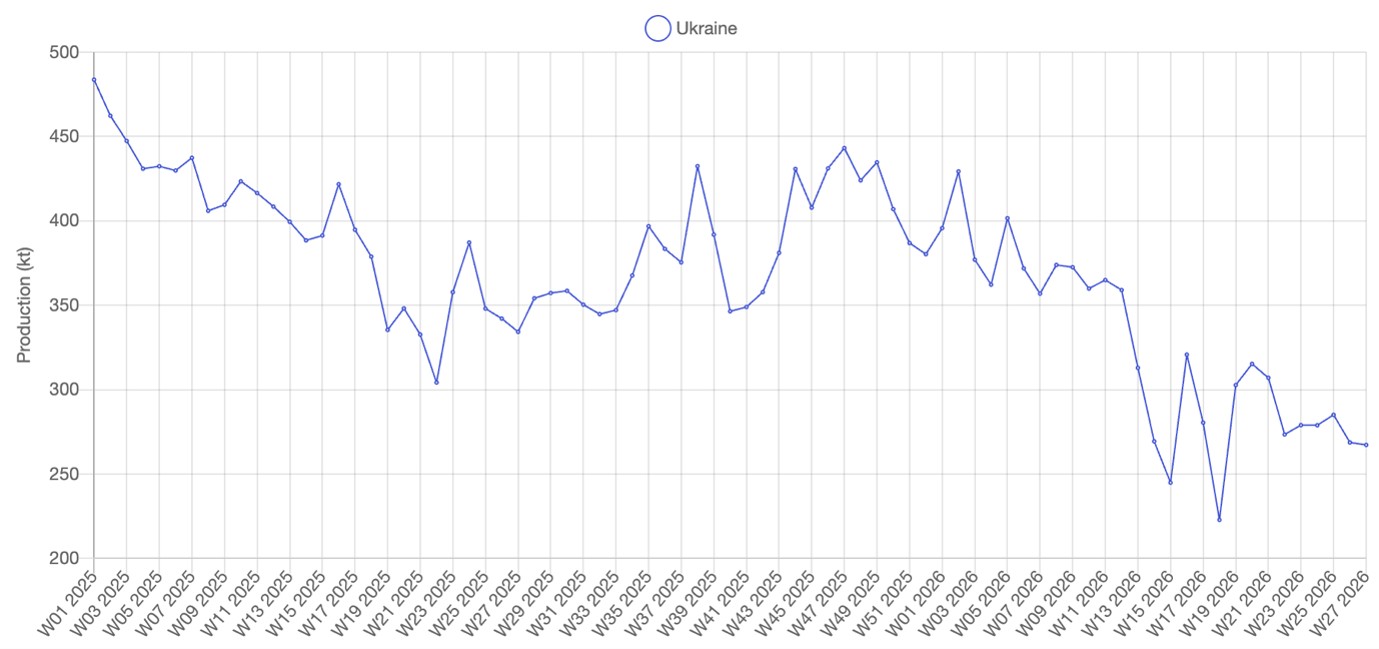

Our July steel update shows steel production activity in Ukraine has receded from its January highs and is now tracking down 18% year to date (to 30-June) versus 2025, according to our SAVANT data.

Fig I – Ukrainian Steel Production (weekly YTD to 30 June 2026)

Ukraine’s steel production already faces ongoing challenges from wartime logistics, power shortages, and the economic impacts of the EU’s Carbon Border Adjustment Mechanism.

Now with the introduction of EU’s new trade regulation known as the tariff and rate quota system (TRQ) uncertainty has increased for Ukraine’s remaining steelmakers. The TRQ restricts annual imports for covered tariff-free steel products to 18.3 million tonnes (down 47% on the 2024 reference). It overrides some aspects of the previous exemptions afforded to Ukraine’s steel imports leaving Ukraine’s situation to be ‘considered’ by the European Commission when allocating country quotas.

The country-specific quotas the EU has allocated Ukraine total only 1.05 million metric tons per year, accounting for less than half of Ukraine’s 2024 steel trade into the EU.

The lack of preferential treatment has drawn criticism from ArcelorMittal Kryvyi Rih and the chief executive of Metinvest, saying the new EU quota system due on 1 July could “kill the Ukrainian steel industry”.

Specifically for the month of June, Earth-i’s SAVANT data shows Ukrainian’s crude steel production down 22% YoY. With frequent electrical outages in the grid, SAVANT is showing that Ukraine’s largest plants, ArcelorMittal Kryvyi Rih (rated at 8Mtpa) and Zaporizhstal Iron and Steel Works (rated at 4.1Mtpa) continue to produce, although only at around 56% and 61% utilisation respectively.

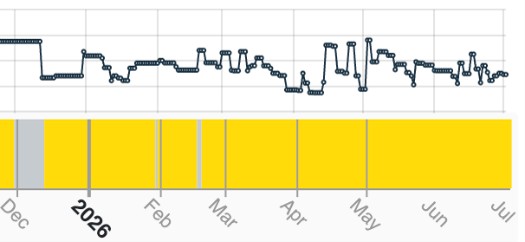

Fig II – SAVANT ArcelorMittal Kryvyi Rih activity chart

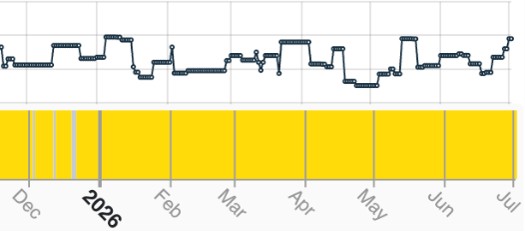

Fig III – SAVANT Zaporizhstal Iron and Steel activity chart

Yellow = active, blue = inactive, grey = no reading

The EU’s new TRQ framework adds further pressure on Ukrainian steelmakers by restricting import volumes just as they face intense, wartime production challenges.