The outbreak of hostilities in Iran that has roiled commodities since the beginning of the month has, of course, been most impactful in oil markets. This is not only because Iran was the world’s 6th largest producer in 2024 at over 4.6 million bbls/day, but because its position on the northern flank of the Persian Gulf confers control over the sea passage for the distribution of five times as many barrels. In addition, over 200 bulk carriers are currently stranded in the Gulf, unable to navigate out to the Arabian Sea for fear of mines, causing far-reaching disruption to global shipping. And for all that the energy transition aspires to reduce the world’s dependence on black gold, petroleum products are still the lifeblood of the global economy.

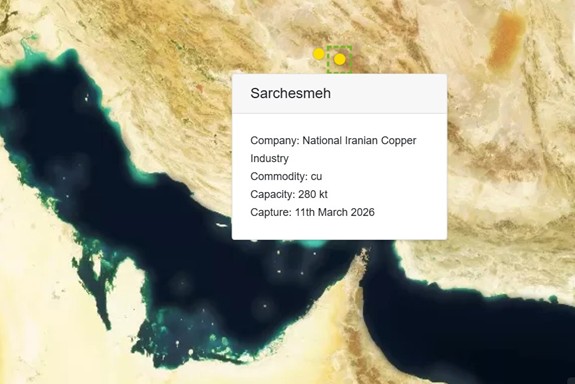

But what of the impact on other parts of the commodities’ complex, including the copper and nickel supply chains monitored by Earth-i’s metals monitoring platform, SAVANT? In terms of first-order effects, SAVANT is showing no impact on the two operating copper smelters in Iran, being the state-owned 280 kt/a Sarchesmeh and 120 kt/a Khatoon Abad plants. These have shown consistent operating profiles since before the air strikes by Israel in June 2025, extending to the present day and consistent with the current messaging from the US President that targets have so far been limited to military installations.

Chart 1: SAVANT monitored copper smelters in Iran

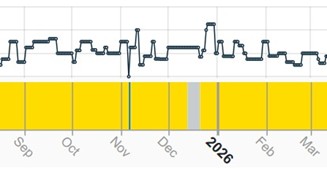

Chart 2: Sarchesmeh (above) and Khatoon Abad (below) smelter activity, September 2025 – Present

Yellow = active, blue = inactive, grey = no reading

Neither would we expect operations to be curtailed by a lack of availability of critical raw material feed, as aluminum smelters like Hydro’s Qatalum in Qatar have been. Here the Norwegian company has been forced to shut down its 648 kt/a JV plant, due to the inability of its gas supplier to guarantee a stable flow following Iranian retaliatory attacks on oil and gas infrastructure in the emirate state.

Second-round effects are most likely to stem from the disruption to global shipping, and primarily the curtailment of supplies like liquid natural gas (LNG). But beyond the energy complex there is the potential for further disruption in other critical elements and, most pertinently for the nickel industry, sulphur. The Middle East produces as much as half of the world’s sulphur as a by-product of the petroleum refining process, which is then shipped around the world to industrial users, with the largest customers being the fertilizer and chemical manufacturing industries.

Importantly, miners who employ leaching processes – of which the nickel industry’s high pressure acid leaching (HPAL) plants are among the most intensive – depend on supplies of sulphur to produce sulphuric acid, the lixiviant that dissolves nickel and cobalt in laterite ores. With the development of nickel-metal hydride (NiMH) batteries for hybrid vehicles that require high purity nickel sulphate (as well as its precursor, nickel matte), HPAL capacity has grown strongly since the beginning of the decade, particularly in Indonesia where companies including PT Vale Indonesia, Zhejiang Huayou, Tsingshan and Ningbo Lygend all have large scale facilities.

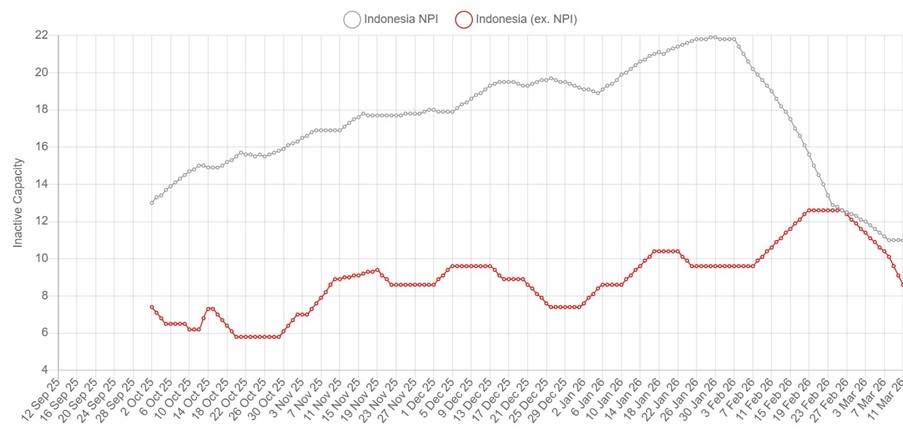

A short war is not expected to impact production at these plants, where operators are believed to have built stockpiles in advance of capacity ramp ups. However, a long war would likely start to assert pressure, increasing the reliance on sourcing nickel units from alternative sources. Companies like PT Vale and Zhejiang Huayou would logically look to their nickel matte producing pyrometallurgical smelters at Sorowako and Weda Bay respectively to make up the shortfall. However, as Chart 3 shows, the SAVANT Indonesia ex. NPI inactive capacity series (a proxy for nickel matte production) is already down in single digits, so that the ability to turn up output to replace lost tonnes from HPAL is limited.

Chart 3: Indonesia NPI and ex. NPI inactive capacity sub-indices, September 2025 – Present

Might a long war therefore be ‘good’ news for copper smelters, able to extract more rent from their own sulpurhuric acid production? This is certainly a possibility with sulphur prices now at multi-year highs, although this would need to be offset by the likelihood of rising power prices in many locations.

But maybe the greater impact for critical mineral industries is going to be a reassessment of the localisation of supply chains in a post-global world. The war has once again highlighted how exposed static infrastructure can be. For now, much of the attention has focused on oil terminals in the region and particularly Kharg Island, Iran’s oil export hub from which more than 90% of the country’s exports originate. But it must also beg the question, what is Vedanta’s appetite to go ahead with its 400,000 t/a smelter/refinery complex and associated 300,00 t/a rod production facility at Ras al Khair in Saudi Arabia? Or indeed MP Materials and Maaden’s to build a rare earths separation and refining facility in the Kingdom? It is hard to believe the events of the last fortnight will not leave a profound legacy.

Chart 4: Proposed location of Vedanta’s copper smelter in Saudi Arabia