With the deadline having expired for the conclusion of Commerce Secretary Lutnick’s Section 232 investigation into the threat to national security associated with copper imports, the market remains split down the middle on whether to expect the imposition of tariffs on refined metal, in addition to the 50% duty already imposed on semi-finished products (‘semis’). It has been almost a year now since those became law. So, ahead of the finalisation of the now overdue report, it begs the question, how successful has existing policy been in encouraging copper processing back onshore?

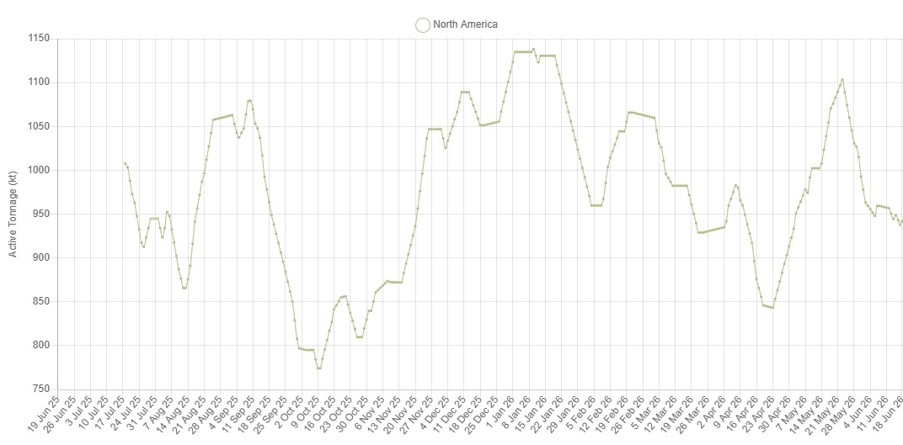

As Chart 1 shows, while there has been significant volatility in the level of active smelting tonnage in the North American market, it is around a stable mean. There has not been a trend upwards and the ‘quick win’ of a restart at the Hayden smelter has not happened, despite the establishment of a solid premium for copper on COMEX above the LME price. Instead, levels of smelting activity in the local market have been most influenced by events at the 320 kt/a Garfield complex and associated Bingham Canyon mine in Utah. In Q3 2025 geotechnical conditions at the mine’s south wall led operator Rio Tinto (Rio) to undertake maintenance shutdowns at both the concentrator and the smelter in September/October, explaining why active tonnage fell from over 1 million tonnes to under 800 kt. Together with the recent breach of the flash-converting furnace that led to an unplanned outage only last month, it has been a challenging 12 months for the operation.

Chart 1: SAVANT active tonnage, N. America, July 2025 – Present

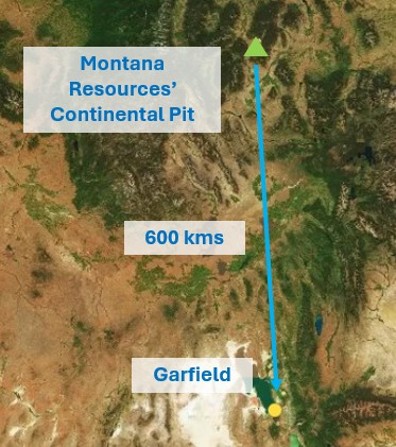

But what is most interesting was the quick rebound in January to new highs that can be explained by a closer look at Rio’s reporting. The Melbourne-headquartered company (rightly) reports production from its own sourced assets at the top line. However, it does note ‘we continue to process third party concentrate to optimise smelter utilisation’ and the amounts are not insignificant. IN the last year (Q3 2025 – Q2 2026), Garfield produced 39.5 kt of copper cathode utilising feed from assets like Montana Resources’ (Montana) Continental Pit. It may be that – at least in the immediacy – those who are most keenly incentivised by both existing and potential duties are smaller operators like Montana, who have the greatest leverage to prices on the COMEX exchange.

Chart 2: Garfield smelter & Continental Pit locations

If the winners so far from tariffs on copper semis may not naturally derive from among the most conspicuous candidates, then the losers should surely be much easier to spot. For Canadian semis manufacturers, like Nexans Canada, their US customers would now be forced to pay an additional 50% for copper wire coming across the border from Montreal. Given the lack of alternative destinations without incurring lengthy, and therefore expensive, ocean freight voyages, this could have been an almost existential issue.

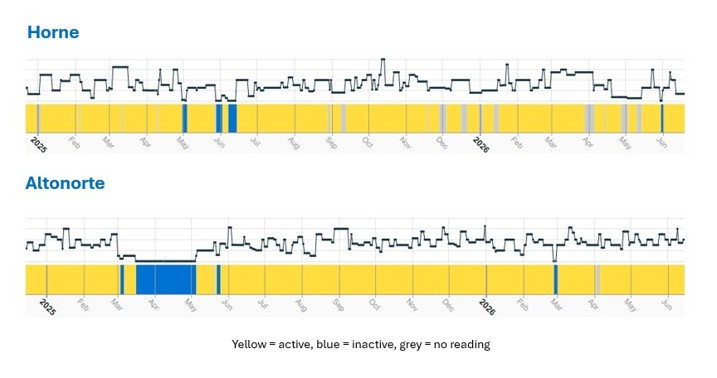

However, looking back into the supply chain, there appears to be a good degree of resilience and adaptability. Nexans take their copper cathode feed from Glencore’s 215 kt/a Horne smelter/refinery complex in Quebec, for which production is not reported individually, but instead grouped under the company’s ‘custom metallurgical assets’. But thanks to SAVANT monitoring we can see that output does not appear to have been impacted (see Chart 3). While there was a dip in divisional level reported output in Q2 2025 due to an (undefined) issue at the Altonorte smelter in Chile, since then output has been consistent at 70 – 80 kt/q.

Chart 3: Horne and Altonorte smelters, January 2025 – Present

Crucially, Horne is a multimetal recycling facility so that rather than the tariff on semis, the more pertinent policy may instead be China’s levies on imports of US scrap – although here again the market has shown its agility so that US exports have largely been re-routed through third countries in Asia. Nontheless, high copper prices always incentivise greater scrap generation so that it is logical to assume there should be more material available to the North American market, with Horne’s consistent operating profile a data point to back this up, despite its location north of the border.

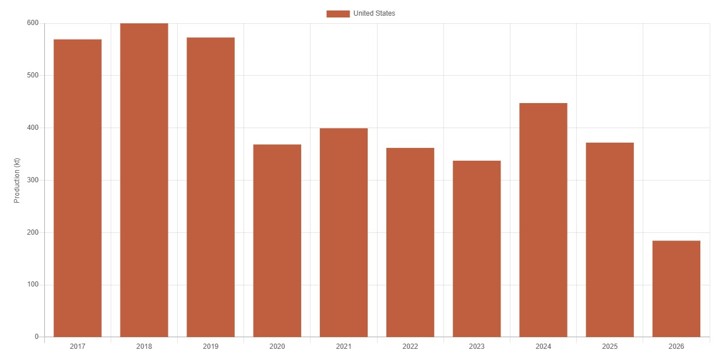

So while junior miners and regional processors are among those that appear to have fared best since the implementation of tariffs on semis in August last year, US copper production has yet to benefit from government policy towards the red metal, with output this year lagging 2024’s recent peak (see Chart 4). Ironically, with the US already home to more than 600,000 tonnes of copper that traders have sent across the Atlantic or shipped up the coast from South America on the arbitrage to the LME, the market would however appear well supplied, even before the possibility of any price-induced demand destruction.

Admittedly this seems unlikely given the current ‘everything AI-related’ frenzy, of which copper has a direct exposure through its usage in data centres. But until there is evidence that these stocks are drawing down, they could serve to dissuade those thinking about adding further processing capacity. With the decision on extending tariffs to refined metal now surely only days away, should we expect a big announcement relating to government funding the domestic copper smelting industry? There are precedents here, particularly in other critical minerals like rare earths. Direct investment might be a better option in this case as well.

Chart 4: SAVANT copper production in beta, USA, 2017 – Present