Our July copper update shows that smelting activity in Q2 2026 followed seasonal patterns according to the latest data from SAVANT, with the percentage of copper smelters registered as inactive rising by 3.3% q/q to 16%.

The second quarter typically sees the lowest level of smelting activity across the calendar year as Chinese smelters take downtime to coincide with a seasonal lull in the production cycle, so that the period is known in the industry as ‘maintenance season’. As such it was little surprise that China, which is home to approximately 50 operational smelters monitored by SAVANT, was the region that saw the greatest q/q rise in inactivity, from 5.5% to 13.9%.

Among the largest plants to take downtime were 300 kt/a Sanmexia in April followed by 400 kt/a Baiyin and 358 kt/a Gansu no. 2, both in May and June respectively. In addition, and as we commented last month, regional acid prices are also playing an important role in smelter economics as headline treatment and refining charges (‘TC/RCs’) remain deep in negative territory.

Fig I: Selected Chinese smelters, H1 2026 – SAVANT data

Yellow = active, blue = inactive, grey = no reading

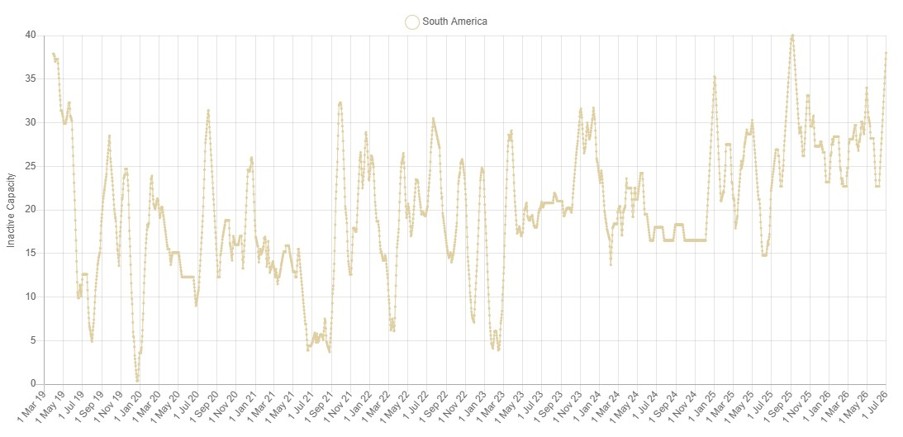

Meanwhile in the Rest of World (RoW), seasonality is generally less pronounced and average smelting activity lower, as proved the case last quarter. Despite the RoW inactive capacity subindex falling by 0.9% q/q, at 17.8% it was still nearly 4% higher than that of China. A significant contributor to this, offsetting higher levels of activity in Europe – the only region where inactivity is in single figures at 8.9% – has been underperformance in South America where the inactive capacity series rose by 4.3% to 31.2%. This was driven by an especially poor showing in Chile which recorded inactivity at 25.4%, a 7.2% increase from Q1 and the highest reading since Q2 2019. This corroborates recently released underwhelming country level manufacturing (-7.2% y/y in May) and copper production (-12.9% y/y) data.

Fig II: SAVANT South America inactive capacity series, 30-day moving average, Q2 2019 – Present

Elsewhere, smelting activity in Asia & Oceania was also weaker compared to previous years, with inactivity averaging 14.7%, 5.4% higher than the three-year average for the second quarter. While there has been a structural impact from the closure of 330 kt/a Isabel Leyte in the Philippines where SAVANT monitoring has not detected any operating signals since March 2025, periods of inactivity at both the 280 kt/a Sarchesmeh and 120 kt/a Khatoon Abad plants in Iran, as well as downtime for rebricking at the 300 kt/a Mount Isa furnace in Australia, have all helped raise the series. In June this was further elevated by a lack of detected operating signals from 354 kt/a Onahama in Japan, a smelter that is set to stop processing copper concentrates by the end of Q1 2027 due to record low TC/RCs.

Fig III: Onahama smelter, H1 2026